Simplify the complexities of rental property taxes. This guide highlights the essential tax documents, strategies for maximizing deductions, and tips to stay compliant while boosting your property's profitability.

By Unknown

Published on 2024-11-17

Owning rental property can be a lucrative investment. It can provide a steady stream of income and potential appreciation. However, it also comes with its share of responsibilities. One of the most critical is managing the tax implications of rental income.

Understanding the tax landscape for rental properties can be complex. It involves navigating a maze of IRS documentation, understanding the nuances of rental income tax, and ensuring compliance with real estate tax laws. This can be daunting, especially for new landlords or those juggling multiple properties.

But fear not. This comprehensive guide is designed to demystify the process. It aims to provide you with a clear understanding of the essential tax documents for rental property owners. It will also offer practical tips to help you manage your real estate taxes effectively.

Whether you're an HOA Board Member, a Condominium Owner, or a Rental Property Investor, this guide is for you. It will help you navigate the complexities of financial management, maintenance, and regulatory compliance for your properties. It will also equip you with the knowledge to maximize the profitability of your investments through proper tax documentation.

We'll delve into the IRS documentation requirements for rental income. We'll explain the relevance of Schedule E and Form 1040 to rental property owners. We'll also explore common rental property expenses that are tax-deductible and how to maximize these deductions.

We'll discuss strategies for dealing with capital gains tax on the sale of rental properties. We'll also touch on the impact of passive activity losses on your tax liabilities. And we'll guide you through the process of property tax assessment and the necessity of issuing 1099 forms to service providers.

We'll also explore the benefits of leveraging technology in managing your taxes. We'll discuss the role of property management software in tracking income and expenses. And we'll highlight the importance of consulting a tax advisor for rental property tax planning.

By the end of this guide, you'll have a comprehensive understanding of the tax landscape for rental properties. You'll be equipped with the knowledge and tools to manage your real estate taxes effectively. And you'll be well on your way to ensuring the smooth operation of your rental properties.

So, let's dive in and start demystifying the world of rental property taxes.

Rental property taxes can be intricate but manageable. Understanding them is key to optimizing your investment returns. There are several components to consider when handling rental property taxes.

The first is rental income tax. This refers to the tax imposed on the income you earn from renting out your property. Knowing how to report this income correctly is crucial.

Real estate taxes also play a significant role. These are taxes based on the assessed value of your property. Being aware of local tax regulations can help you plan financially.

Tax deductions are another important aspect. They can significantly reduce your taxable income. Common deductions include mortgage interest, property management fees, and repair costs.

Depreciation is a vital concept in rental property taxation. It allows you to recover the cost of your property over time. Understanding how depreciation works can provide substantial tax benefits.

Handling a property sale introduces capital gains tax. This tax arises from the profit gained from selling your property. Planning ahead can help mitigate its impact.

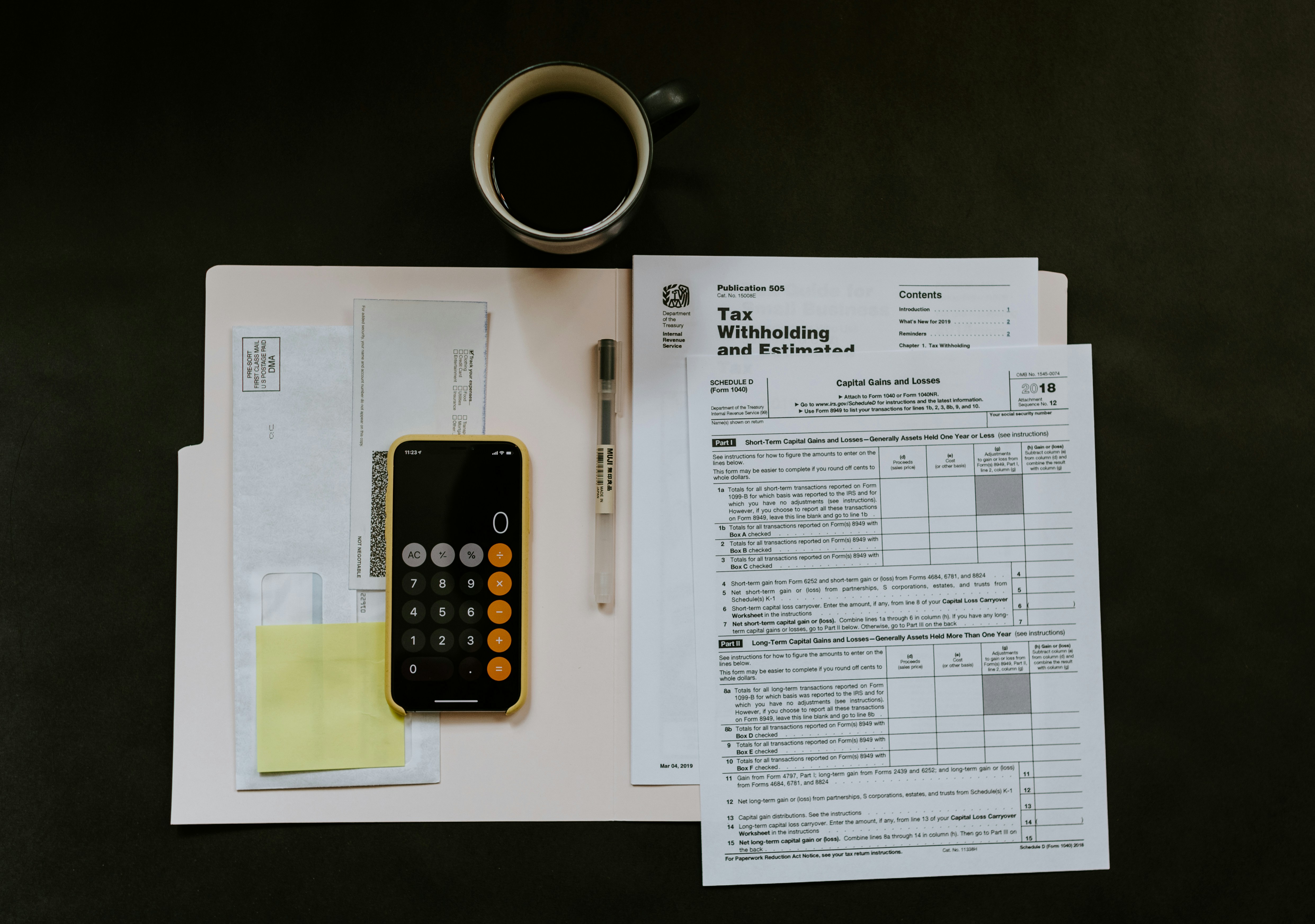

Lastly, the IRS provides various forms for tax reporting. Familiarity with essential forms like Schedule E and Form 1040 is necessary. They are integral in documenting and filing your rental income and expenses.

Tax compliance is essential for every rental property owner. It's not just about avoiding penalties. It's about ensuring your operations run smoothly and legally.

Failure to comply can lead to legal complications and financial loss. Ignorance of tax laws is not an excuse. Keeping up-to-date with changes in tax regulations is vital.

Staying compliant builds trust with your tenants and partners. It reflects professionalism and diligence. This can enhance your reputation and business relationships.

Compliance also opens doors to financial benefits. Proper management of your tax documents can lead to deductions. These deductions can lower your taxable income and increase profitability.

To effectively manage rental property taxes, understanding key tax terms is important. Here's a list of fundamental concepts to familiarize yourself with:

Understanding these terms will aid in navigating the tax landscape effectively. Rental income must be reported accurately to avoid penalties. Depreciation plays a huge role in reducing taxable income over time.

Capital gains can significantly impact your finances when selling a property. Planning and understanding the implications is crucial. Passive activity losses can offset other income, which is beneficial for tax planning.

Property tax assessment informs your real estate tax obligations. Being proactive about assessments can prevent surprises. Issuing 1099 forms ensures compliance with reporting requirements for services rendered.

By mastering these terms, you'll be better equipped to manage your rental property taxes.

Managing rental property taxes involves understanding and using the correct IRS documentation. Proper filing ensures compliance and can help optimize your tax benefits. Key documents include Schedule E and Form 1040.

Schedule E is integral for reporting rental income and expenses. It's the primary form rental property owners use to detail income earned and costs incurred.

Form 1040 serves as the main form for individual tax returns. It consolidates all income types, including those from rental properties, to determine overall taxable income.

Other important IRS forms might come into play, depending on your situation. For example, you might need a 1099 form if you pay contractors more than $600 annually.

Here's a list of essential IRS documentation for rental income:

Staying organized with these forms helps simplify the tax process. It also ensures that you take advantage of all available tax benefits.

Accurate documentation minimizes errors and protects against audits. Consistently maintaining records prevents last-minute scrambles during tax season.

Schedule E is the backbone of rental income tax reporting. It provides a comprehensive breakdown of income and expenses. This form lets you list revenue from all rental activities.

Expenses reported on Schedule E can include maintenance, insurance, and utilities. Each expense category helps reduce your taxable rental income. Accurately recording these details ensures you receive rightful deductions.

Schedule E also accommodates depreciation. This critical component lowers taxable income by accounting for the property's wear and tear. Knowing how to calculate depreciation effectively can yield significant tax savings.

Filling out Schedule E requires attention to detail. Inaccurate reporting can lead to audits or penalties, so precision is crucial. Keeping thorough records throughout the year makes this process smoother and less stressful.

Additionally, Schedule E allows for the reporting of passive income losses. These losses can offset income from other sources, providing further tax relief. Understanding passive activity loss limitations is key for proper reporting.

Form 1040 is the foundational document for all individual taxpayers. It consolidates various income sources, including salary, dividends, and rental income. Ensuring accuracy on this form is paramount to effective tax filing.

Rental income reported on Schedule E feeds into Form 1040. This inclusion affects your overall taxable income and tax rate. Understanding how each piece fits into the broader picture aids in strategic tax planning.

Form 1040 also includes itemized deductions. If you choose to itemize, make sure you include all relevant rental expenses. This step can help reduce your overall taxable income significantly.

Beyond rental specifics, Form 1040 accounts for credits you might be eligible for. Examples include energy-efficient improvements or credits for maintaining historic properties. These credits can further ease your tax burden.

Staying updated with any changes to Form 1040 is essential. Tax laws and forms frequently evolve, impacting how you report income and deductions. Regularly consulting updated IRS guidelines can prevent costly mistakes.

Understanding deductible expenses is vital for rental property owners. These deductions can significantly reduce taxable income, enhancing your investment's profitability. Knowing which expenses qualify ensures you're not leaving money on the table.

Deductible expenses encompass a variety of costs. They cover ordinary and necessary expenses incurred in managing and maintaining rental properties. Accurate record-keeping is crucial for substantiating these claims during tax filing.

Maintenance and Repairs are common deductions. Routine repairs to keep properties habitable qualify, but improvements may not. It's important to distinguish between the two for tax purposes.

Interest payments, especially on mortgages, are a major deductible expense. These deductions can considerably lower your taxable income. It's crucial to maintain detailed records of interest payments for accurate reporting.

Operational costs such as utilities, insurance, and management fees also qualify. Each plays a role in maintaining property value and functionality. Tracking these expenses provides an edge during tax time.

Here's a markdown list of deductible expenses to consider:

Travel expenses are often overlooked. If you manage properties in different locations, costs related to travel may be deductible. This inclusion can further expand your deductions.

Legal and professional fees associated with rental activities also qualify. Engaging accountants or legal advisors incurs costs that might be deductible. Confirm with a tax advisor to ensure compliance with IRS regulations.

Every rental property owner should know about common deductible expenses. These expenses can vary widely depending on the nature of your property. Deductions directly impact your bottom line by lowering taxable income.

Property taxes are a significant deductible expense. Paying these taxes is a necessary part of property ownership. Keeping receipts and statements ensures you're accurately claiming this deduction.

Advertising costs for finding tenants qualify as deductions. Any expense tied to promoting vacancies can be written off. Maintain all receipts and invoices to back up your claims during tax time.

Another area to consider is insurance premiums. Protecting your property against loss is essential, and the IRS allows deductions for these premiums. Documenting annual premiums is a must for accurate tax reporting.

Depreciation, a non-cash expense, can lead to substantial deductions. It accounts for property wear and tear over time. Calculating depreciation correctly plays a key role in tax strategy.

Here's a markdown list of more common deductible expenses:

Travel-related costs for property management duties qualify as deductions. Whether it's showing properties or making repairs, these costs add up. Track mileage and transportation expenses meticulously.

Office supplies and small equipment specifically used for rental property operations count too. It's easy to overlook these minor expenses, but they add up over the tax year. Recording these costs contributes to maximizing deductions.

Depreciation is a key tax consideration for property owners. It allows you to deduct the cost of property over its useful life. Understanding this concept is crucial for efficient tax planning.

The IRS provides specific guidelines for calculating depreciation. Real property has different depreciation rules than personal property. Familiarizing yourself with these distinctions optimizes your tax position.

Residential rental properties are typically depreciated over 27.5 years. This period reflects the property's useful life for accounting purposes. Ensure you're following the correct schedule to maximize deductions.

Land itself isn't depreciable, only the structures and certain improvements on it. Identifying these assets accurately affects your depreciation calculations.

Depreciation begins when a property is ready and available for rental, not necessarily when it's occupied. Starting this timeline correctly maximizes your benefits.

Overstating or understating depreciation can lead to tax issues. Correctly maintaining records and calculations is essential. This diligence provides a clear financial picture and prepares you for potential audits.

Capital gains and passive activity losses present unique challenges. Selling a rental property can trigger capital gains tax. Knowing how this works is vital for financial planning.

Capital gains are the profits realized from selling your property. They're taxed differently based on various factors. Understanding these nuances helps minimize tax liabilities.

Passive activity losses (PALs) affect rental property tax calculations. These losses occur when expenses exceed income. The IRS places restrictions on deducting these losses.

Navigating these complexities is crucial for property investors. Proper planning can mitigate the impact of capital gains and PALs. Leveraging available strategies maximizes financial benefits.

Effective tax management involves a clear understanding of these elements. Take proactive measures to optimize tax outcomes. Professional guidance may be necessary for intricate situations.

Managing capital gains tax requires strategic planning. Rental property sales can lead to significant tax events. Employing smart strategies mitigates the impact of these gains.

The holding period of the property influences your tax rate. Long-term gains, from properties held over a year, are usually taxed at a lower rate. Strategic timing of property sales can benefit your tax position.

Utilizing Section 1031 exchanges allows deferral of capital gains tax. These exchanges involve swapping one property for another similar one. It's a powerful tool for reinvesting and managing tax liabilities.

Cost basis adjustments are essential when calculating gains. This includes accounting for improvements made to the property. Accurate adjustment ensures you don't overpay on taxes.

Consulting a tax advisor can offer tailored strategies for capital gains tax. Every property situation is unique. Expert advice aligns your tax plan with your investment goals.

Passive activity losses are a common concern for landlords. These occur when total expenses surpass rental income. Understanding their impact is crucial for managing your tax obligations.

The IRS limits the ability to offset passive losses against non-passive income. This regulation can result in unused losses. Tracking and documenting these losses is important for future deductions.

Real estate professionals have an advantage regarding PALs. They might qualify for exemptions, allowing better use of these losses. Determining your status as a real estate professional can affect your tax strategy.

Unused PALs can be carried forward to offset future gains. This carryover can be beneficial in following years. Proper documentation ensures you're ready to utilize these losses when eligible.

Understanding how passive activity losses integrate into your overall tax picture is vital. It helps in forecasting future tax liabilities. Regular consultation with a tax advisor optimizes your use of PALs.

Understanding property tax assessments and issuing 1099 forms is crucial for rental property owners. These elements are significant in managing financial responsibilities.

Property tax assessments determine the amount of tax you'll pay annually. They're based on the assessed value of your property. Understanding this process can save you significant amounts over time.

Meanwhile, 1099 forms are essential for recording payments made to service providers. Proper issuance of these forms ensures compliance with IRS regulations.

Both assessments and 1099 forms require attention to detail. They play key roles in maintaining your property's financial health. Awareness of these requirements can prevent complications and maximize efficiency.

Staying informed about how these processes work is essential. Regularly review property assessments and your obligations related to 1099 forms. A proactive approach can prevent financial discrepancies.

Property tax assessment is a systematic process. It evaluates your property's value to determine your annual tax responsibility. Understanding this process helps ensure fair taxation.

Local governments conduct these assessments. They typically involve reviewing recent home sales, property improvements, and market trends. These factors contribute to the assessed value.

Assessments generally occur annually or biannually. However, some fluctuations in property value might trigger a reassessment. It's wise to stay informed about upcoming assessments in your area.

Knowing how assessments work can help in challenging or appealing unfair assessments. With the right evidence, you can effectively advocate for a fair valuation. This can significantly impact your annual tax expenses.

1099 forms are pivotal in documenting business expenses. They're necessary when paying more than $600 to independent contractors or service providers in a year. Ensuring accurate issuance is crucial for tax compliance.

These forms help the IRS track income paid to non-employees. This makes them an integral part of your tax documentation strategy. Recording these transactions prevents misunderstandings and penalties during audits.

Issuing 1099 forms requires specific information from recipients. This includes their taxpayer identification number. Maintaining thorough records simplifies the form issuance process.

Prepare your 1099 forms early to meet the IRS deadlines. Sending these forms to both the recipient and the IRS ensures complete transparency. This practice supports better financial and legal management of your rental properties.

Technology is a powerful ally in managing rental property taxes. With the right tools, you can simplify complex tax tasks and reduce errors. Embracing technology can streamline your tax preparation process.

Digital tools offer numerous benefits for property owners. They enhance accuracy by automating calculations and simplifying document storage. This not only saves time but also improves compliance.

Utilizing technology can aid in organizing your financial records. Access to digital versions of receipts and invoices makes filing taxes more efficient. This technology helps keep everything in one place for quick access.

Automation features in software can reduce the risk of human error. By generating reports and reminders, technology ensures you don't miss important deadlines. This proactive approach fosters effective financial management.

Investing in the right software is essential. Consider solutions that meet your specific needs, from tracking income to preparing reports. Technology is your partner in navigating the complexities of tax season with ease.

Property management software plays a vital role in tax preparation. It automates many aspects of the process, ensuring efficiency and accuracy. This software is indispensable for modern rental property management.

One of the key benefits is automated record-keeping. This feature stores all financial transactions in an organized manner, aiding compliance. With everything in place, preparing taxes becomes less daunting.

These tools also provide thorough reporting capabilities. Generating reports on rental income and expenses offers valuable insights into your financial status. This information is crucial for effective tax planning.

Finally, property management software offers features that enhance decision-making. With detailed analytics, you can make informed tax decisions to optimize deductions. This strategic approach to tax preparation enhances profitability and compliance.

Navigating the intricacies of rental property taxation can be overwhelming. This is where a tax advisor can add significant value. A professional can offer tailored advice to maximize tax benefits and ensure compliance.

It's essential for property owners to work with an experienced tax advisor. They help you stay updated on tax law changes and avoid costly penalties. This expertise is invaluable for optimizing your tax strategy.

For audit planning, preparedness is key. Organizing your records and having accurate documentation can ease potential audits. A tax advisor can guide you through setting up efficient record-keeping systems.

Proactive planning with a tax expert can mitigate risks. Advisors assist in identifying areas of concern before they escalate. This strategic foresight provides peace of mind for property owners.

Advisors also support in deciphering complex tax regulations. With their help, understanding your rights and responsibilities becomes manageable. They simplify the process, making tax season more predictable.

Regular consultations can also prevent financial missteps. Establishing a routine with your tax advisor ensures ongoing compliance and financial health. This continued partnership benefits rental property operations.

The complexity of tax laws necessitates professional guidance. Tax advisors bring expertise that is crucial for rental property owners. Their insights aid in making informed financial decisions.

Relying on a tax professional ensures compliance. Advisors know the intricacies of tax codes and can prevent errors. This support is essential for avoiding fines and complications.

They also bring a strategic edge to tax planning. By evaluating your financial situation, advisors recommend deductions and credits. This personalized approach optimizes tax savings.

Engaging a tax advisor builds a proactive defense against audits. With their advice, you prepare your records accurately. This preparation is key for facing potential scrutiny from tax authorities.

Tax audits can be daunting, but preparation reduces stress. Building a systematic approach to organize records is crucial. Having detailed documentation ready is your best defense.

Start by ensuring that all income and expenses are recorded. Maintain clear records to support every financial transaction. This attention to detail can significantly affect audit outcomes.

A tax advisor can guide you in audit readiness. They help identify potential areas of concern in advance. This foresight is invaluable for addressing issues before they arise.

Additionally, understanding audit procedures is essential. Familiarize yourself with the process to know what to expect. This knowledge empowers you to respond confidently if audited.

Managing tax documents is crucial for successful rental property accounting. Proper documentation ensures you can substantiate claims and deductions during tax season. This practice also helps in keeping your finances organized.

Rental property owners should implement an efficient system for storing tax documents. This system aids in tracking income, expenses, and potential deductions throughout the year. It simplifies tax preparation when deadlines approach.

Essential records play a vital role in minimizing tax liabilities. Maintaining accurate records allows you to maximize deductions and avoid issues with the IRS. They are your main tool for optimizing tax returns.

Moreover, well-organized tax documents provide insights into your property's financial health. Analyzing these records helps identify trends and areas for improvement. This analysis is essential for strategic decision-making.

Incorporating technology into your document management process can enhance efficiency. Digital storage solutions offer easy access to your tax information. They provide a reliable backup in case of physical loss.

Being proactive in rental property accounting involves planning ahead. Regularly updating your records ensures they accurately reflect your property's performance. This ongoing diligence is crucial for long-term success.

Keeping comprehensive records is essential for effective tax filing. You need to maintain both income and expense records to accurately report your earnings. This documentation is also necessary for supporting your tax deductions.

Important documents to retain include:

Maintaining these records substantiates your claims during tax season. They enable you to accurately report income and expenses to the IRS. Additionally, they safeguard against discrepancies in your tax filings.

Proper documentation also provides clarity into your property's cash flow. It highlights what expenses are tax-deductible, allowing you to benefit from available deductions. This understanding is crucial for tax optimization.

Digital copies of receipts and statements can enhance your record-keeping. Using digital tools minimizes paper clutter and streamlines access to important documents. This step also aids in easy retrieval during audits or tax preparation.

Consistent organization is key to managing your records effectively. Regularly update your files to ensure they reflect current transactions and obligations. This habit supports accurate and timely tax filings.

Developing robust accounting practices is vital for rental property owners. It not only simplifies tax preparation but also enhances financial visibility. Following best practices in accounting can lead to better decision-making and efficiency.

First, maintaining separate accounts for each property ensures clear financial management. It avoids mixing personal and business expenses, reducing complications in tax filing. This separation is crucial for precise tracking of property-specific income and costs.

Regular reconciliations of your accounts are another essential practice. They help identify discrepancies early and ensure records match bank statements. Regular checks prevent errors from becoming significant issues over time.

Implementing accounting software tailored to rental properties can streamline operations. It automates repetitive tasks like invoicing and expense tracking. This automation saves time and reduces manual errors.

Engaging a professional accountant familiar with rental properties can be beneficial. Their expertise ensures compliance with tax regulations and improves financial accuracy. They offer insights that can refine your financial strategies.

Overall, diligent accounting practices prepare you for any financial contingencies. Staying organized and proactive lays the groundwork for efficient tax management. It sets the stage for maximizing profits and minimizing tax liabilities.

For rental property owners, implementing advanced tax strategies is vital for reducing liabilities. By employing strategic planning, you can protect and enhance your investments. This approach demands a keen understanding of available tax benefits.

Effective tax strategies require a holistic view of your entire financial situation. By considering all aspects of your property portfolio, you can identify opportunities for tax savings. This comprehensive analysis is crucial for capitalizing on all potential deductions.

One proven strategy involves timing your income and expenses to your advantage. Deferring income or accelerating expenses can reduce taxable income in a high-tax year. This timing can lead to substantial savings on your tax bill.

Regularly reviewing property depreciation schedules is another key tactic. Understanding depreciation allows you to maximize deductions across the lifespan of your property. It's a powerful tool in reducing taxable income.

Strategic planning also involves considering tax implications before making property transactions. Thoughtful management of property sales and purchases can optimize your tax situation. This foresight helps in preserving profits and mitigating taxes.

Being proactive about tax planning and seeking professional advice is crucial. A tax advisor can provide insights into optimizing your strategy. Their expertise helps navigate complex tax regulations and improve your financial outcomes.

To minimize tax liability, rental property owners must engage in strategic planning. By carefully considering the timing and structure of transactions, you can optimize tax outcomes. This planning involves a deep dive into your current and future financial conditions.

Revisiting your property's operating expenses is a starting point. By documenting and categorizing expenses thoroughly, you can identify additional deductions. This activity often uncovers overlooked opportunities to lower taxable income.

Another aspect to consider is the method of property ownership. Structuring your investments under different entities can have tax advantages. This setup may offer liability protection while optimizing your tax situation.

Charitable deductions related to property can also reduce your tax burden. Donating property or using it for philanthropic activities can result in significant tax breaks. This option not only benefits your bottom line but also contributes positively to society.

Stay informed about changes in tax laws that may impact your strategies. Regularly consulting with a tax professional can keep you updated on law revisions. This vigilance ensures that your planning remains effective and compliant.

Cost segregation studies offer valuable benefits for property owners looking to optimize taxes. These studies break down property costs into various components. This detailed analysis accelerates depreciation, providing immediate tax relief.

By reallocating costs into shorter depreciation periods, you can access upfront tax deductions. This shift boosts cash flow, which is crucial for reinvestment and growth. It's an essential tactic for those looking to enhance their property's financial performance.

Engaging a tax professional is key when pursuing a cost segregation study. They have the expertise to accurately classify assets and realize the maximum tax benefits. Their involvement ensures compliance with IRS rules and optimizes your tax position.

Beyond cost segregation, exploring energy-efficient upgrades can also yield tax benefits. Certain improvements may qualify for tax credits or deductions, reducing overall costs. These enhancements not only save money but also add long-term property value.

Investors should also consider conducting regular reviews of their tax strategies. Adapting to changes in personal circumstances or tax law adjustments is crucial. Consistent evaluation helps you maintain effective strategies and maximize benefits year after year.

In summary, leveraging advanced techniques like cost segregation can significantly impact tax liabilities. It's essential for rental property owners to adopt a proactive approach. Such strategies ensure they're benefiting fully from available tax advantages.

Preparing for tax season as a rental property owner can seem daunting. However, a systematic approach can make this task manageable. With a clear strategy, you can ensure accuracy and maximize your tax benefits.

First, it's important to organize all your documentation. Collect income statements, receipts, and previous tax returns. Having everything in one place will simplify the process.

Next, review the current tax laws and regulations. Changes in the tax code could affect your filing. Staying informed allows you to leverage any new opportunities.

Consider using property management software to manage and track expenses. This software can help automate tasks and provide accurate financial reports. Access to real-time data ensures you're never caught off-guard.

Seek advice from a qualified tax advisor. Their expertise can provide clarity and identify savings you might miss. Professional insight helps navigate complicated tax regulations.

Utilize checklists to ensure nothing is overlooked. Tracking each step prevents common mistakes during preparation. This diligence is key to a smooth tax season.

Here's a simplified checklist for tax preparation:

Lastly, schedule your tax filing early. Avoid the stress of last-minute submissions by planning ahead. Timely filing minimizes errors and allows time to address any issues.

Navigating tax preparation involves several critical steps. Begin by documenting all rental income and keeping meticulous records. These records form the basis of your tax filings and ensure compliance.

Next, categorize expenses accurately. This step will maximize deductions and reduce taxable income. Categories might include repairs, management fees, and utility costs.

Evaluate your depreciation schedule. Adjust it for any new improvements or significant repairs made during the year. Proper depreciation lessens your taxable income effectively.

Assess potential tax credits available for energy-efficient upgrades. These credits can substantially lower your tax liability. They offer an incentive for making environmentally-conscious property enhancements.

Double-check that all required forms are completed. Missing documentation can lead to delays or penalties. Accuracy here is crucial for seamless tax filing.

Regularly update and back up your financial information. Inaccurate or lost records could result in higher liabilities. Using cloud storage provides a secure way to maintain your data.

Here's a concise breakdown of essential tax preparation steps:

Remaining organized throughout the year aids in a smoother tax preparation. Consistency in record-keeping proves valuable in minimizing stress come tax season.

Filing your tax return requires attention to detail. Many pitfalls can arise from neglecting small yet critical elements. Awareness of these aspects can save you from costly errors.

One common mistake is underestimating rental income. All income, including payments from tenants and additional fees, must be reported. Underreporting can lead to audits and penalties.

Neglecting to capitalize on all available deductions is another error. Ensure all eligible expenses are included, and consider consulting a professional. They can help identify less obvious deductions.

Beware of filing late or missing deadlines. Late submissions could incur penalties and interest charges. Timely filing is essential for maintaining good standing with tax authorities.

Double-check personal information for accuracy. Errors in your name, address, or identification numbers can cause issues. These mistakes can delay refunds and necessitate follow-ups.

Always keep copies of your tax return and all associated documents. These records can be crucial if discrepancies arise later. Proper filing provides a reference for future tax planning.

In conclusion, approach your tax filing with care and precision. Avoiding common pitfalls is as vital as pursuing deductions. Taking these steps positions you for a successful tax season.

Successfully managing rental property taxes hinges on organization and knowledge. Meticulous record-keeping is essential to maintaining tax compliance. This practice not only avoids penalties but also positions you for potential audits.

Tax compliance ensures that you meet all legal obligations. It safeguards against discrepancies and reinforces the integrity of your financial reporting. Regular audits of your records can further enhance accuracy and compliance.

Maximizing benefits is about leveraging the available deductions and credits. Understanding what qualifies can significantly lower your taxable income. Utilize tools such as property management software to track deductions systematically.

Consulting professionals, like tax advisors, can reveal savings opportunities you might miss. Their expertise guides strategic decision-making. When tax season arrives, you'll feel prepared and confident.

In conclusion, a proactive approach to tax management combines detailed documentation with expert insight. By ensuring compliance and focusing on available benefits, you'll optimize your tax position. This strategy can enhance the profitability of your rental property investments.

Navigating rental property taxes can be complex, but numerous resources and tools can help streamline the process. Effective use of these resources can simplify tax preparation and ensure you stay compliant.

Consider exploring online tax filing software designed for property owners. These platforms often offer guided assistance and automated calculations. They are an excellent tool for keeping your tax affairs in check.

Also, make use of educational resources such as webinars and guides. Many organizations offer free materials to enhance your understanding of real estate taxes. Here's a list of helpful resources to consider:

Using these resources wisely can make tax management less daunting and more efficient.